Blog

How Much Cash Will You Get After Selling Your HDB? Here’s the Truth About Sale Proceeds

Published 2 May 2025

TL;DR / Summary:

– Your HDB cash proceeds = Selling price – Outstanding loan – CPF refund (incl. 2.5% accrued interest) – Fees.

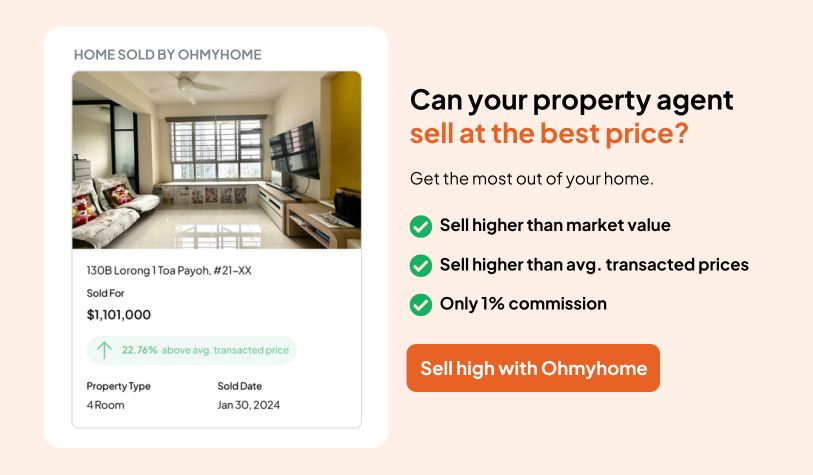

– A flat sold at $380,000 can leave you with only ~$40k–$60k cash after loan, CPF, and selling costs are deducted.

– CPF refunds (including grants and interest) go back to your CPF Ordinary Account, not your bank, – usually within 15 working days after completion.

– You receive your actual cash on resale completion day, after all deductions are settled.

– If proceeds aren’t enough to refund CPF, you usually don’t need to top up in cash as long as the flat was sold at market value.

Many first-time home sellers in Singapore are surprised when their HDB flat sells for a good price, yet the cash they actually receive is much lower. For example, you might sell your flat for $380,000 but walk away with only a fraction of that, say around $40,000 in cash.

This happens because your selling price is first used to settle your home loan, CPF refunds, and fees before any cash is paid to you.

So, if you’re wondering, “How much cash proceeds will I get after selling my HDB?” or “How much do I need to return to CPF?”, this guide breaks it down step-by-step, from CPF refunds and accrued interest to calculating your final cash in hand.

Table of Contents:

- First, Do You Know the Real Value of Your HDB?

- What Are HDB Cash Proceeds?

- When Will I Get My Cash Proceeds After Selling My HDB Flat?

- How to Calculate Sales Proceeds From Sale of HDB Flat?

- How Much Do You Need to Return to CPF?

- What If My HDB Sale Proceeds Aren’t Enough to Refund the CPF Amount Used?

- Selling a Fully Paid HDB Flat: What You Still Owe

- Do You Need to Pay a Resale Levy?

- No Time to Do the Math? UseAI to Calculate Your Potential Cash Proceeds For You

- Have a Financial Plan Before Selling Your HDB Flat

- Sell Your HDB Fast and At the Best Price!

- Frequently Asked Questions About Cash Proceeds After Selling HDB

First, Do You Know the Real Value of Your HDB?

Before you even list your HDB for sale, you can get a free indicative HDB valuation with HomerAI. While this isn’t the official appraisal by HDB, it is a good estimate of how high you can sell your home. And with HomerAI, you’ll get monthly updates on any changes in your HDB valuation. Did I mention it’s free?

Get an instant valuation for your home Access property insights and AI tools to maximise your property's potential and sell it fast Floor - Unit Property Type Home Type - Postal Code Get FREE valuation

What Are HDB Cash Proceeds?

HDB cash proceeds are the actual cash you’ll get in hand after selling your HDB flat. But before that happens, a few things need to be settled first, like paying off your remaining home loan and returning any CPF savings you used (plus accrued interest) back to your CPF account. You’ll also need to cover legal fees and other costs, if any.

Whatever’s left after all that? That’s your HDB cash proceeds. It’s the money you can use for your next home, to top up savings, or simply take a breather before your next move.

When Will I Get My Cash Proceeds After Selling My HDB Flat?

You will receive your cash proceeds on the day your HDB resale is finalised, on the resale completion appointment. It is usually issued as a cashier’s order that you can deposit into your bank account. This is when the sale is finalised and all deductions (loan repayment, CPF refund obligations, fees) have been processed.

In contrast, any CPF amounts you used for your flat are usually refunded to your CPF Ordinary Account within 15 working days after completion. These funds are not part of the immediate cash you take home.

If ownership is joint, HDB will issue the cashier’s order in joint names or split according to ownership shares.

How to Calculate Sales Proceeds From Sale of HDB Flat?

To calculate your HDB sales proceeds, subtract your outstanding loan, CPF refund (including accrued interest), and transaction fees from your final selling price.

Quick formula overview:

Sales Proceeds = Selling Price – Outstanding Loan – CPF Refund (Principal + Accrued Interest) – Transaction Fees

Below is a simple step-by-step breakdown to help you estimate your HDB sales proceeds more accurately.

Step 1: Determine Your Gross Selling Price

Start with the agreed selling price of your HDB flat. This is the amount your buyer pays before any deductions are made.

To estimate how much your flat can realistically sell for, check recent resale transactions on the Housing & Development Board portal to see what similar units in your area have sold for.

To speed things up, you can also use HomerAI to get a free, instant property valuation based on current market data.

Example: If your flat sells for $650,000, this is your gross selling price.

Step 2: Subtract Your Outstanding Home Loan

Next, deduct any remaining housing loan balance (HDB or bank loan). This amount is paid directly to your lender when your sale completes.

To get the most accurate figure, request a loan redemption statement from the Housing & Development Board or your bank. This shows your exact outstanding balance, including interest up to a projected completion date.

Keep in mind that this amount changes daily due to interest, so it’s best to request an updated statement closer to your sale completion.

Step 3: Refund the CPF Used (Plus Accrued Interest)

If you used CPF savings to buy your HDB flat, you must refund that amount when you sell, along with accrued interest, which represents what your CPF would have earned if it had stayed in your account.

This refund is returned to your CPF Ordinary Account, not paid to you in cash. As a result, your actual cash proceeds may be lower than expected, even if your flat sells at a good price.

You can check your estimated CPF refund amount through the Central Provident Fund Board website before completing your sale.

Step 4: Deduct Transaction Fees

Lastly, factor in the costs that come with selling your HDB flat, such as:

- Agent commission (if you’re using an agent)

- Legal conveyancing fees

- Miscellaneous administrative charges

These may look small compared to your loan or CPF refund, but together, they still chip away at your final cash proceeds. Including them early helps you avoid surprises and gives you a clearer picture of what you’ll actually walk away with after the sale.

Example Breakdown of HDB Sale Proceeds Calculation

Here’s an example of how HDB sale proceeds are calculated, based on Mr and Mrs Lim’s 4-bedroom flat in Jurong East:

Details

Amount (SGD)

Selling Price

$380,000

Outstanding Loan Amount (HDB)

$180,000

CPF Refund (Mr Lim)

$70,000

CPF Refund (Mrs Lim)

$70,000

Resale Levy (if any)

NA

Total Cash Proceeds from HDB

$60,000

Legal Conveyancing Fee (HDB)

$500*

Ohmyhome Agent Fee (incl. 7% GST)

1% of selling price + GST= $4,066

HDB Admin Fee

$80

Net HDB Cash Proceeds

$55,354

*HDB legal fee is estimated, and the final amount is subjected to HDB’s calculation.

Ohmyhome Tip: To skip manual calculations, use HomerAI to get your estimated cash proceeds after selling your HDB instantly, based on your flat type, location, and CPF usage.

Get an instant valuation for your home Access property insights and AI tools to maximise your property's potential and sell it fast Floor - Unit Property Type Home Type - Postal Code Get FREE valuation

How Much Do You Need to Return to CPF?

Every dollar withdrawn from your CPF Ordinary Account for your HDB must be returned, plus 2.5% accrued interest per annum. This includes:

- Stamp duties, legal fees paid via CPF.

- Monthly instalments paid using CPF

- CPF housing grants

What If My HDB Sale Proceeds Aren’t Enough to Refund the CPF Amount Used?

If your HDB sale proceeds are not enough to fully refund the CPF you used (including accrued interest), you usually do not need to top up the shortfall in cash, as long as you sold your flat at market value and did not deliberately under-sell.

In this case, the Central Provident Fund Board will take whatever proceeds are available, and the remaining shortfall is waived.

To avoid surprises, check your estimated CPF refund early via the CPF website.

Selling a Fully Paid HDB Flat: What You Still Owe

Even if you’ve fully cleared your HDB loan, CPF refunds can still significantly reduce your cash proceeds. This often surprises sellers who assume a “fully paid” flat means they’ll receive most of the selling price in cash.

What matters isn’t just whether your loan is cleared, it’s how much CPF you used over the years, including grants and accrued interest.

Do You Need to Pay a Resale Levy?

You only need to pay a resale levy if you’re buying another subsidised HDB flat (such as a BTO or Executive Condominium). The resale levy is paid in cash or deducted from your HDB sale proceeds, it cannot be paid using CPF.

No Time to Do the Math? UseAI to Calculate Your Potential Cash Proceeds For You

With HomerAI, you can get an automatic calculation of your potential cash proceeds, as well as your affordability for your next home. You can access these two calculators for free on HomerAI.

Have a Financial Plan Before Selling Your HDB Flat

Selling your HDB flat to purchase a new property is not merely “upgrading”. Not really. There are a lot of long-term factors that could affect your financial situation in the future, which could either make or break your bank, as well as your housing options.

From the interests of home loans and grants to the miscellaneous costs and fees, it would be best to work out a thorough financial calculation with a trusted advisor before plunging into anything.

Sell Your HDB Fast and At the Best Price!

Sell your home in Singapore for a high price in no time, hassle-free. Starting at 1% + GST of selling price. Drop us a message on WhatsApp or chat with us via our Live Chat at the bottom, right-hand corner of the screen.

Our Super Agents are CEA-certified and among the Top 1% in Singapore. With more than 8,000 happy customers served, we’ve garnered 4-star ratings on both Facebook and Google! We go in-depth about what you can expect when you engage an Ohmyhome HDB Seller Agent.

Frequently Asked Questions About Cash Proceeds After Selling HDB

1. What happens when you sell your HDB flat?

When you sell your HDB flat, the resale process begins with registering your intent to sell via the HDB Resale Portal. From there, you can list your flat, negotiate with buyers, and issue the Option to Purchase (OTP) once you secure a serious buyer.

After the buyer exercises the OTP, both parties submit the resale application to HDB, which usually takes about eight weeks to be approved, followed by a completion appointment.

At completion, your HDB sale proceeds are first used to settle key obligations, including:

- Paying off your outstanding home loan (if any)

- Refunding CPF monies used plus accrued interest

- Settling your resale levy (if applicable)

- Covering legal, admin, and agent fees

Whatever remains becomes your cash proceeds after selling your HDB, which is transferred to your bank account shortly after the sale is completed.

2. How to calculate cash proceeds from sale of HDB flat?

To calculate your cash proceeds after selling HDB, you’ll need to deduct the following from your selling price:

- Outstanding home loan balance (if any)

- CPF refund – all CPF monies used for the flat, including housing grants, plus accrued interest

- Resale levy (if applicable)

- Legal and administrative fees

- Property agent commission

Cash proceeds = Selling Price – Outstanding Loan – CPF Refund – Fees – Resale Levy

3. How long does it take to get CPF refund after selling house?

After your HDB sale completion, your CPF refund is typically processed within two to three weeks. The refunded amount (including accrued interest) will be credited directly to your CPF Ordinary Account (OA).

Remember: Your cash proceeds from selling HDB will only be released after CPF and loan obligations are settled. You can check the status of your refund via the CPF portal after the sale is finalised.