Blog

7 Must-Know Tips When Moving From HDB to Condo in Singapore

Published 1 July 2025

Thinking of selling your HDB flat and buying a condo? You’re not alone. Many HDB homeowners start dreaming about their condo move long before their Minimum Occupation Period (MOP) is up. By the time you’re eligible, the excitement is real but so is the complexity. Reading the market, sorting your finances, and timing your sale and purchase correctly can make the difference between a smooth move and a costly one.

At Ohmyhome, we’ve helped over 14,500 families make this transition, and we’ve outlined 7 tips below to help you out as well.

Table of Contents:

- 1. Understand the Market Before You Upgrade from HDB to Condo

- 2. Check Your Eligibility to Sell

- 3. Know the HDB Selling Process

- 4. Plan the Right Timing

- 5. Do the Math on Your Finances

- 6. Explore Your Loan Options

- 7. Don’t Do it Alone – Get Advice from Professionals

- Frequently Asked Questions About Moving From HDB to Condo

1. Understand the Market Before You Upgrade from HDB to Condo

Know when to sell and when to buy property, based on real data.

The property market is always moving, and so should your strategy. Knowing when to sell and buy can help you maximise your HDB sale and make a smarter condo purchase.

HDB Resale Market

Resale HDB prices are expected to rise by 2% to 6% for the full year of 2026. That’s a significant cooldown from previous years, and the reason is simple: more supply has started coming in. With 13,480 flats reaching MOP in 2026, nearly double last year’s figure, buyers now have more options and less pressure to overbid. Prices are still rising, just at a steadier, more manageable pace.

Condominium Market

Private home prices are projected to rise around 3% in 2026, driven by demand for new launches even as new supply tightens. New condos continue to cost more than resale units on a per square foot basis, though resale condos often offer larger floor areas for the same price point.

Still, it’s not a straightforward decision for everyone. The cost gap between HDB flats and private homes remains significant, and affordability continues to be a real barrier for many flat owners.

Moving from HDB to condo may make sense for some, particularly those sitting on strong equity in well-located estates, but it’s not a one-size-fits-all move. Your budget, lifestyle needs, and long-term plans should guide your next step.

2. Check Your Eligibility to Sell

Your MOP is the key.

Before you get too excited about moving from HDB to condo, make sure you’re legally allowed to sell your flat. The most important factor is your Minimum Occupation Period (MOP), usually five years from the date you collect your keys, not from your purchase or completion date.

A common misconception? That you can sell as soon as your mortgage is paid off. Unfortunately, that’s not the case; the MOP still applies even if the loan is fully cleared.

If your MOP ends in 2026 or has already passed, now’s the perfect time to start planning your next move.

💡 Tip: You can check your exact MOP status quickly by logging in to My HDBPage.

3. Know the HDB Selling Process

It’s more than just listing and waiting; timing and strategy matter.

Here’s how selling your HDB flat works:

- Register your intent to sell on the HDB Resale Portal

- Market your unit with quality photos and accurate pricing

- Host viewings and engage interested buyers

- Negotiate and accept the best offer

- Submit HDB resale application

- Finalise the sale and hand over the keys

You don’t need to do it all alone. Selling your HDB and moving to a condo is a big move, but with the right support, it doesn’t have to be stressful.

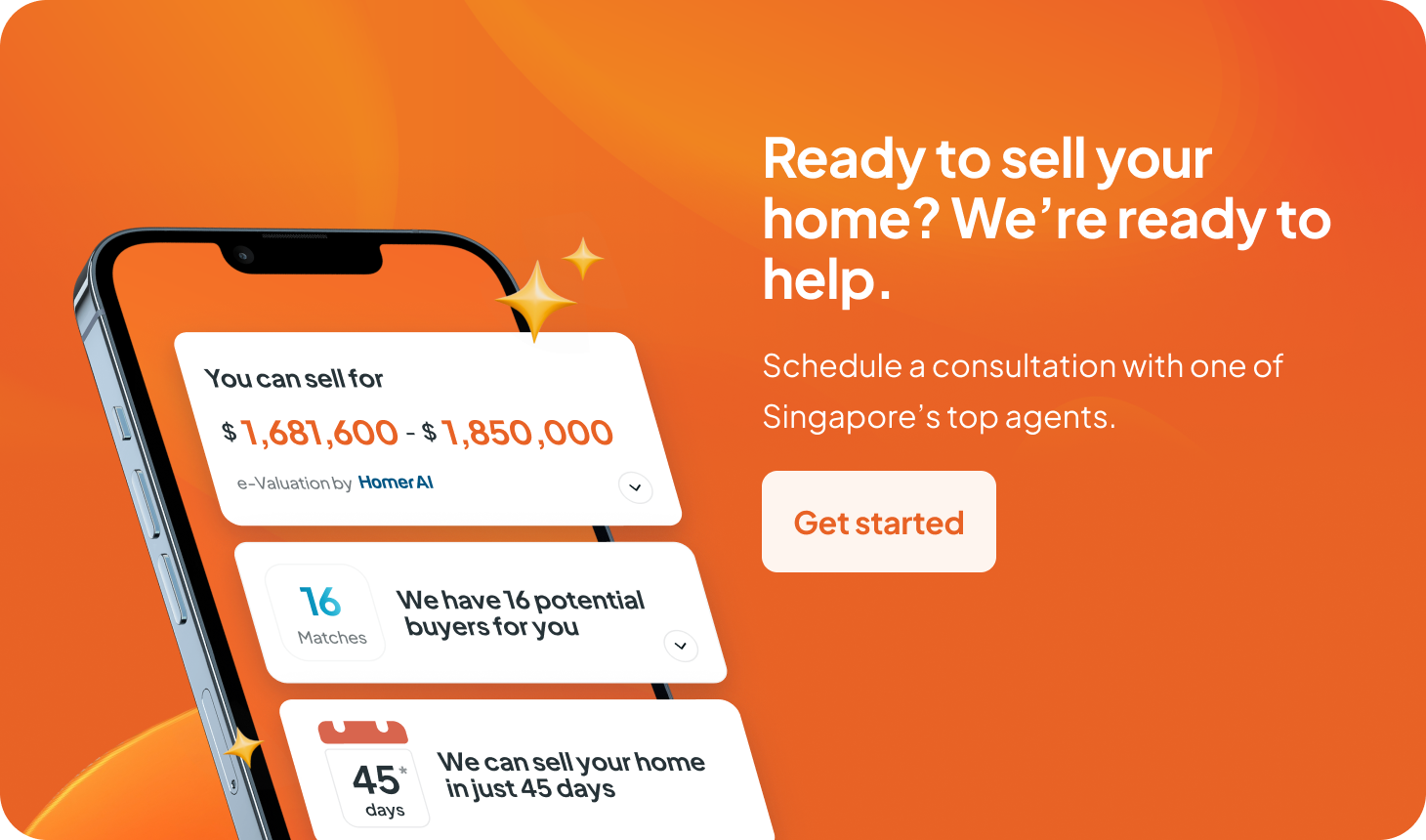

Engage an Ohmyhome super agent and we’ll guide you through every step, from pricing and marketing all the way through to negotiations and handover.

4. Plan the Right Timing

Should you sell or buy first? The answer depends on your situation.

Both options have pros and cons:

Option

Pros

Cons

Sell First

Know exactly how much cash you’ll have

May need temporary housing or a bridging loan

Buy First

Secure your dream home early

Risk of juggling two mortgages

💡 Keep in mind: You can request an Extension of Stay (EOS) for up to 3 months in your HDB after the sale, but only if you’ve already bought your next home and are waiting to collect the keys or finish renovations. The EOS doesn’t give you extra time to house hunt, so make sure you’ve planned your next steps before relying on it.

Use MATCH technology to receive curated property listings tailored to your budget, preferred location, and move-in timeline, directly on your phone.

5. Do the Math on Your Finances

You need to know both what you’re getting and what you’ll need to spend.

Before you dive in, get a clear picture of your finances, what you’ll receive from your HDB sale, and what you’ll need to budget for your condo.

Selling HDB

- Cash Proceeds: Use the HomerAI Cash Proceeds Calculator to estimate how much you’ll receive after repaying your mortgage and refunding the CPF used for the purchase.

- Outstanding Loans: Ensure that you account for any outstanding loan balances, including accrued CPF interest.

Buying a Condo

- Buyer’s Stamp Duty (BSD): This applies to all property purchases and is based on the purchase price or market value, whichever is higher.

- Additional Buyer’s Stamp Duty (ABSD): If you’re buying a condo before selling your HDB, you may need to pay ABSD upfront, unless you’re eligible for remission.

- CPF Usage: You can use your CPF savings to pay for the new condo, but there are limits based on the property’s valuation.

Use HomerAI to get a personalised breakdown of your finances, from cash proceeds to upfront costs, all in real-time.

6. Explore Your Loan Options

You can borrow up to 75%; however, you’ll need cash for the rest.

So, if you’re not buying fully in cash, here’s what to know:

- First, you can borrow up to 75% of the purchase price.

- Next, you must pay at least 5% in cash and 20% via CPF or cash.

Use the HomerAI Affordability Calculator to see what you can comfortably afford based on your income.

7. Don’t Do it Alone – Get Advice from Professionals

Selling and buying at the same time? It can be complex. That’s why Ohmyhome doesn’t just assign you one agent; we give you an entire support team.

With Ohmyhome, you’re not left to figure it out solo. We provide:

- Super Agents who transact 11x more than average

- MATCH technology to pair you with the right condos

- HomerAI tools to plan your sale and next purchase

- Customer support from sales to renovation

At Ohmyhome, we’re all about making home transactions simple, stress-free, and successful. We sell over 63% of our homes within 7 days, and 73% fetch above-average prices.

You’ve worked hard for your home. Now, it’s time to make it work harder for you.

Let’s make your move together.

When you’re ready to go from planning to doing, drop us a message on WhatsApp or chat live with us. From selling your HDB to buying a condo, you’ll never walk alone. With Ohmyhome, you’ve got a team that truly cares.

Frequently Asked Questions About Moving From HDB to Condo

1. Can I buy a condo if I have a HDB?

Yes, but there’s an important condition. If at least one flat owner is a Singapore citizen, you can hold both an HDB and a condo at the same time, but buying the condo while still owning your HDB means paying 20% ABSD upfront. If all owners are Permanent Residents, you’ll need to sell the HDB after buying private property. Most homeowners choose to sell their HDB first, which means no ABSD applies on the condo purchase.

2. Which is better, HDB or condo?

It depends on your budget, lifestyle, and long-term goals. HDB flats are more affordable and come with grants, while condos offer facilities and potentially higher capital gains. Neither is universally better. The right choice comes down to what you can comfortably afford and what suits your life stage.

3. Can I rent out my HDB and stay in a condo?

Yes, once your HDB flat has cleared its five-year MOP, you can rent out the whole unit and stay in a condo instead. Just keep in mind that you’ll need HDB’s approval before doing so, and eligibility conditions apply at the time of application.